Brownfield is the new Greenfield

OWL brings deep expertise in financial and tax due diligence, with a strong track record advising investors,

Read now

Ensuring success in international mergers and acquisitions requires a deep understanding of the differences

Read now

Europe’s first generation of onshore wind and solar PV – built in the 2000s and early 2010s – is approaching the end of their design life. 74 GW of onshore wind will face a repower/ life‑extension/ decommission decision by 2030, while “boom‑era” solar fleets in core markets are now in the repowering window.

The most compelling advantage is the strategic value of existing sites: grid connections are scarce and often the binding constraint. Securing a new grid connection for a greenfield project in Germany or Spain can take five to eight years, while repowering can typically retain and upgrade existing connections.

Policy is moving in the same direction: under RED III, repowering permitting is capped at six months in Renewables Acceleration Areas and ≤1 year outside, with grid-connection decisions within three months (subject to national transposition and project specifics).

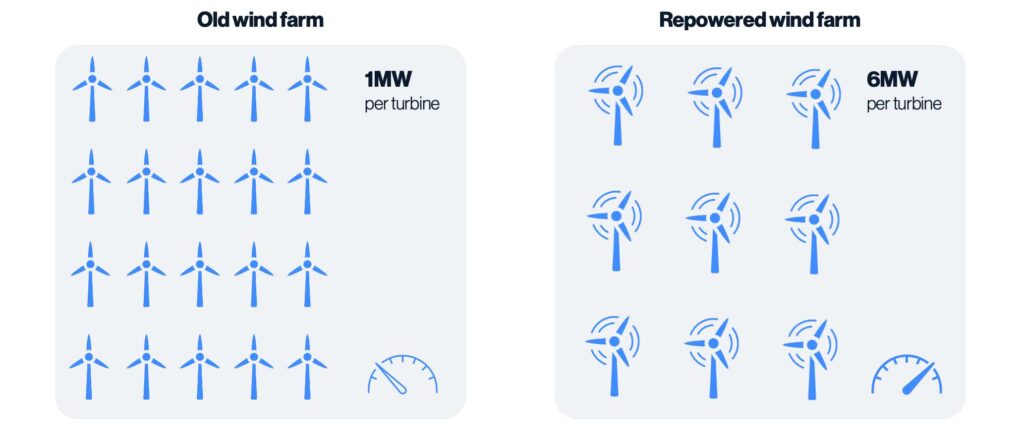

Less infrastructure. More energy.

Technology has shifted the frontier. Modern onshore turbines (5–7 MW, rotors >160m) can deliver multiples of early-2000s output. Repowering typically reduces turbine count by ~1/3, while more than doubling typically reduces turbine count by ~1/3, while more than doubling installed capacity and tripling electricity output on average. Solar follows similar logic: module efficiency has roughly doubled since 2010, and inverter end-of-life (10–15 years) often triggers broader upgrades.

Comparison

Source: WindEurope, Eight Advisory Analysis

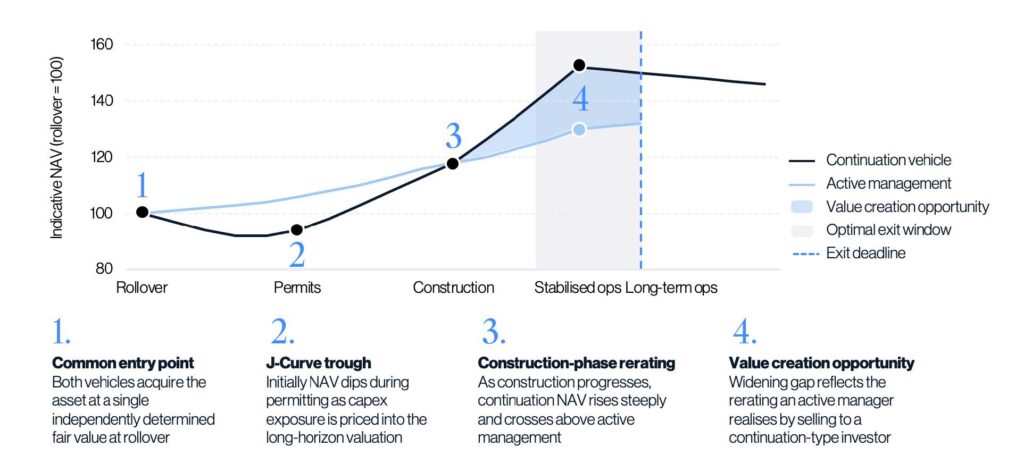

Despite the scale, only a fraction is expected to be fully repowered by 2030: ~16 GW of full repowerings are projected across Europe 2026–2030, versus the 74 GW cohort facing decisions. The bottleneck is not principally economics or technology, but the mismatch between repowering portfolios and conventional SPV-by-SPV project finance: cash flows cannot be pooled across assets, deepening the J-curve and increasing all-in financing costs and execution risk.

The paper describes two complementary equity approaches:

Net Asset Value (NAV) development across repowering investment models

Source: Eight Advisory Analysis

Find out more in our latest whitepaper.

Please let us know if you have a question, want to leave a

comment, or need further information on Eight International