2026 Restructuring Trends Report

Ensuring success in international mergers and acquisitions requires a deep understanding of the differences

Read now

As the private equity industry continues to evolve, technology-related challenges have become central

Read now

Our Restructuring Trends Report leverages our cross-border experience to deliver practical insights into the shifting restructuring landscape. It explores where pressure is intensifying, how capital is adapting, and what management teams need to prioritise to successfully navigate complexity and achieve sustainable turnaround outcomes. In today’s environment, geopolitical disruptions, including the war in the Middle East, are no longer isolated events, but structural forces influencing corporate decision-making for the long term. As these pressures accelerate, companies that adapt effectively will be those combining financial discipline, operational resilience and strategic agility, treating transformation not as a one-off initiative, but as an ongoing capability.

Restructuring is now structural rather than cyclical, driven by sustained cost pressures, limited access to financing, and ongoing geopolitical disruption.

The conflict in the Middle East is further intensifying these challenges, reshaping global supply chains and increasing energy costs, maritime insurance premiums and shipping lead times, adding uncertainty in an already low-visibility environment for management teams.

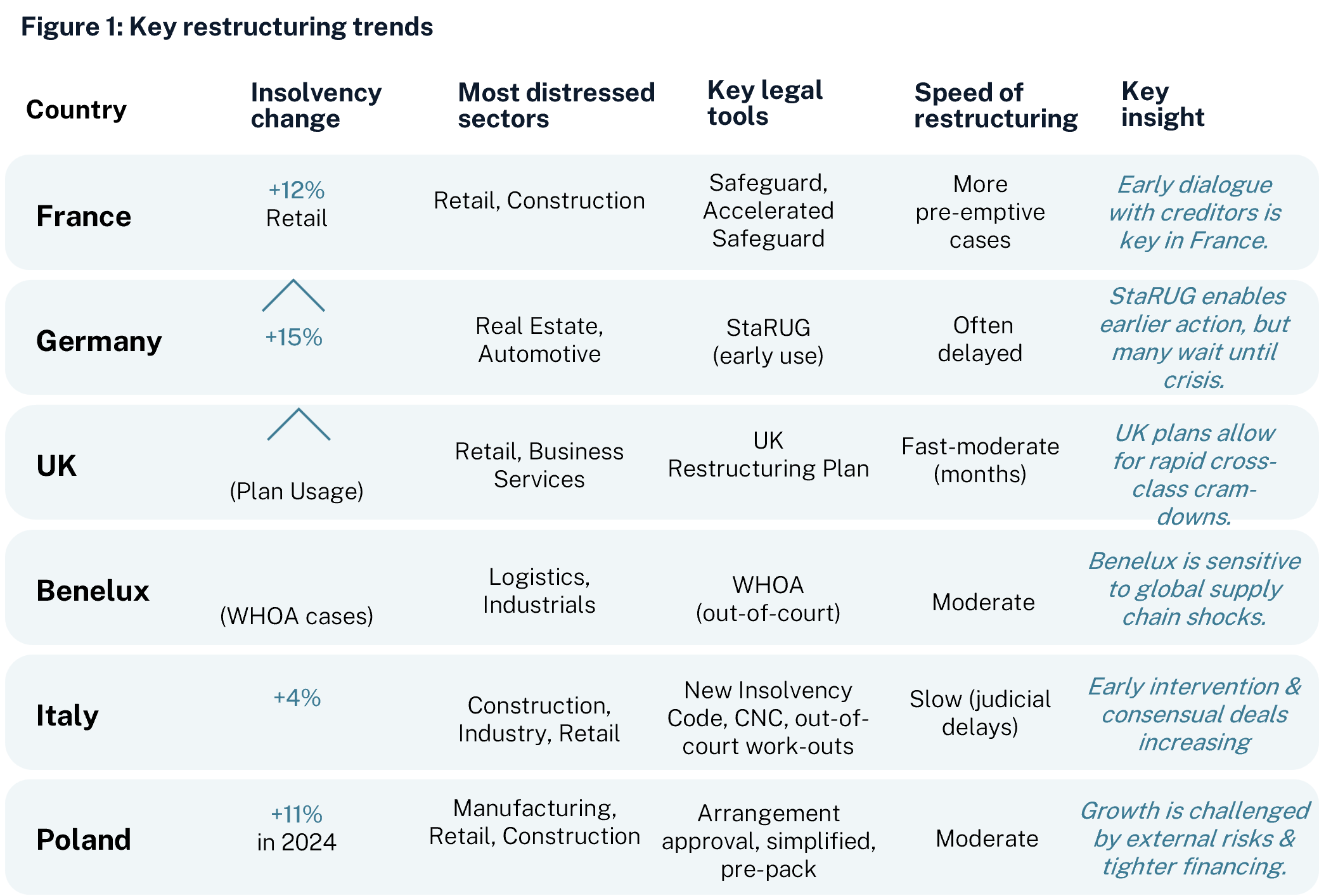

This trend is clearly visible in insolvency data across Europe. Corporate failures are rising significantly, with France surpassing 68,000 insolvencies in 2025 and notable increases in Germany, the UK, Poland, Benelux and Italy. Financial distress is now widespread, affecting multiple sectors and geographies.

At the same time, the restructuring ecosystem continues to evolve. Private credit funds and alternative capital providers are playing an increasingly central role, stepping in where banks are more cautious and often taking a more active, solution-driven approach. In parallel, legal frameworks are enabling earlier intervention.

Regulatory developments are accelerating pre-emptive restructuring, with tools such as StaRUG (Germany), WHOA (Netherlands), Safeguard (France) and the UK Restructuring Plan facilitating earlier, out-of-court processes.

Sector challenges are becoming more structural, particularly in retail, construction, real estate, business services and industrials, all facing sustained margin pressure and transformation demands.

Distressed M&A activity is increasing but remains highly selective. Bolt-on acquisitions and carve-outs dominate, while valuation gaps and cautious investor sentiment continue to limit broader deal flow.

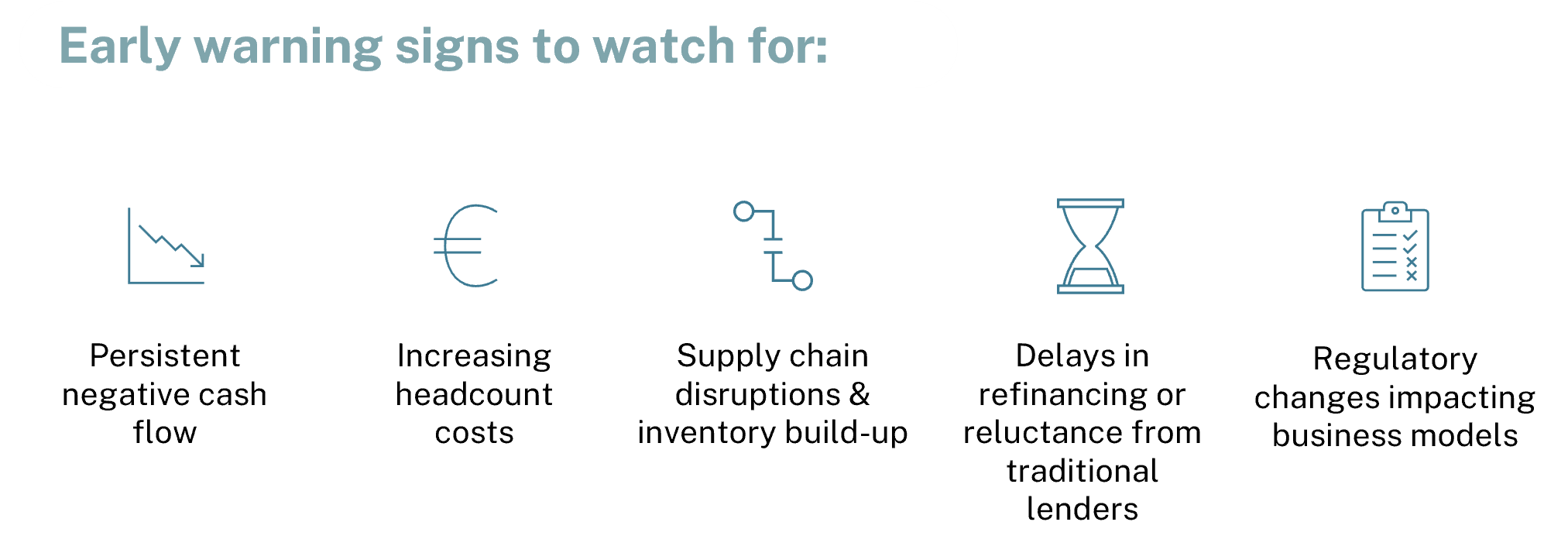

AI and digitalisation are becoming key resilience drivers. Organisations leveraging data-driven monitoring and automation demonstrate stronger adaptability and improved early-warning capabilities.

Companies that succeed act early and decisively, resetting strategic priorities, accelerating decision-making (80/20 principle), and maintaining transparent stakeholder engagement to preserve value.

How we can support you

At Eight International, we support companies facing underperformance – from commercial turnaround situations to severe financial distress. With more than 40 partners and directors dedicated to restructuring across Europe, our multidisciplinary teams combine financial, operational and strategic expertise to deliver pragmatic, results-oriented solutions.

From initial diagnostics through to execution, we design and implement turnaround plans that stabilise operations, protect value and accelerate recovery.

Please let us know if you have a question, want to leave a

comment, or need further information on Eight International